10 Jul The Evolution of AI Agents: Transforming Community Banking with Directlink

AI agents were prominently highlighted at Google’s annual I/O conference, where the unveiling of their AI agent, Astra, showcased the potential to interact seamlessly with consumers through audio and video. Similarly, OpenAI’s GPT-4o model is also considered to be an AI agent, underscoring the rapid advancements in this field.

As noted by Melissa Heikkilä in her article, “What are AI Agents?” published in the MIT Technology Review, tech companies are heavily investing in the development of AI agents, envisioning systems that can autonomously manage a wide range of tasks, much like a human assistant.

Understanding AI Agents

AI agents are AI models and algorithms designed to make decisions and perform tasks in a dynamic environment autonomously. Jim Fan, a senior research scientist at Nvidia, emphasizes that the ultimate vision for AI agents is a system capable of executing a vast array of tasks, much like a human assistant. These tasks range from booking vacations and managing calendars to suggesting plans based on weather forecasts and making lists.In essence, AI agents are multi-modal entities that can process language, audio, and visual inputs. This versatility allows them to function across various platforms, from smartphones to desktop computers, making them an invaluable asset in both personal and professional settings.

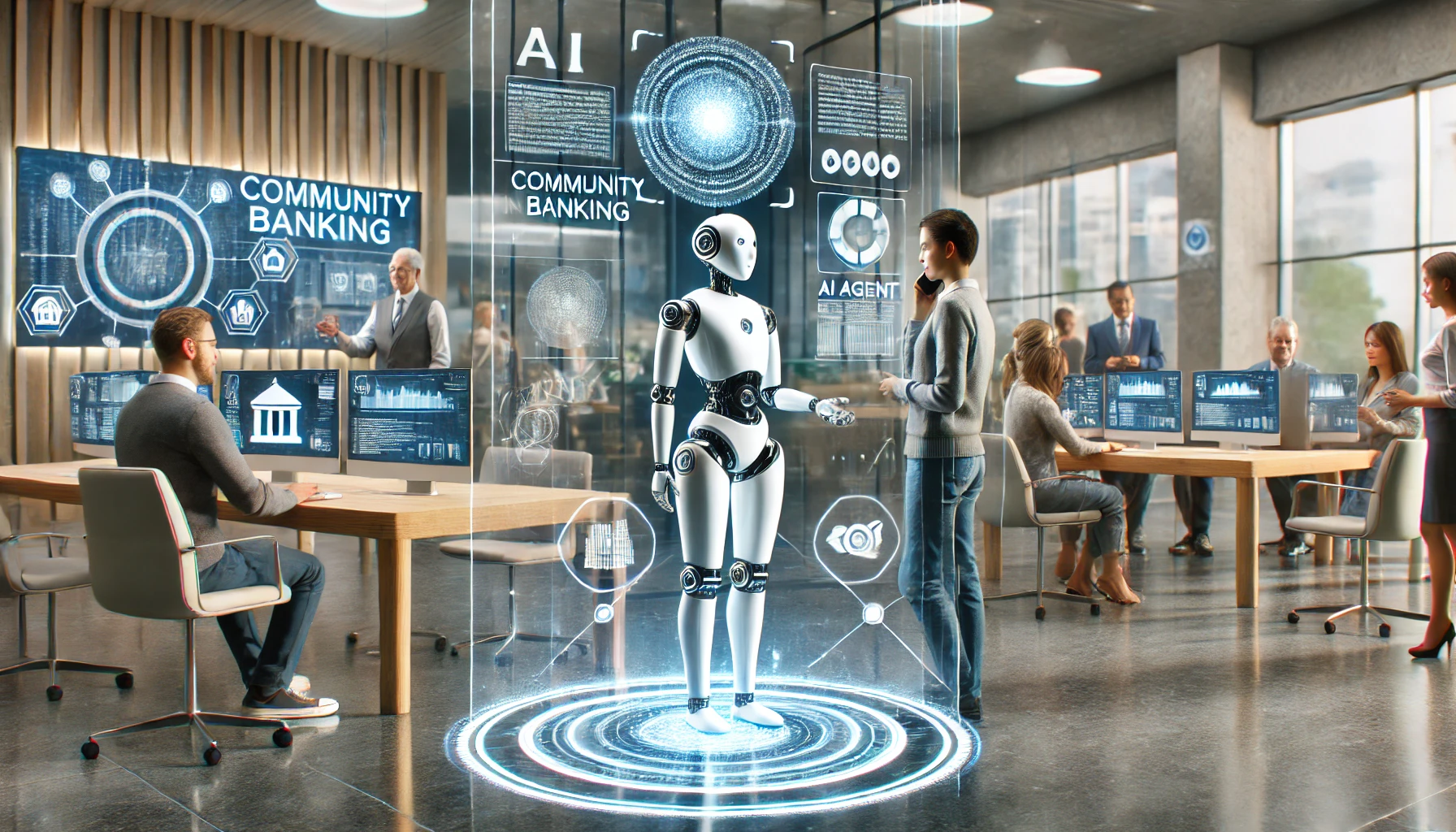

AI Agents in Community Banking

At Directlink, we recognize the transformative potential of AI agents in enhancing the operations of community banks and credit unions. The integration of AI agents can revolutionize customer interactions, streamline backend processes, and provide personalized banking experiences.

Enhancing Customer Service

One of the most significant benefits of AI agents in community banking is the enhancement of customer service. AI agents can handle a myriad of customer inquiries, providing real-time responses and solutions. This not only improves customer satisfaction but also allows human agents to focus on more complex tasks that require a personal touch.

Streamlining Operations

AI agents can automate routine tasks, such as processing loan applications, managing accounts, and conducting compliance checks. This automation leads to increased efficiency, reduced error rates, and significant cost savings for community banks. By taking over these repetitive tasks, AI agents free up valuable time for bank employees to engage in more strategic and high-value activities.

Personalized Banking Experiences

With their ability to analyze vast amounts of data, AI agents can offer highly personalized banking experiences. They can predict customer needs, recommend financial products, and provide tailored advice. For instance, an AI agent can analyze a customer’s spending habits and suggest personalized savings plans or investment opportunities, fostering deeper customer relationships and loyalty.

The Future of AI Agents for Community Financial Institutions

The future of AI agents for community banks and credit unions is promising. As AI technology continues to advance, AI agents will become even more sophisticated, capable of handling increasingly complex tasks and providing more nuanced and personalized services. The ongoing research and development in this field, driven by institutions like the Rochester Institute of Technology, will pave the way for innovative applications in banking and beyond.

At Directlink, we are committed to staying at the forefront of these advancements. Our AI-driven solutions are designed to empower community banks and credit unions, helping them navigate the evolving landscape of banking with confidence and agility. By embracing AI agents, we can transform the way community banks operate, delivering exceptional value to both customers and institutions.

This rise of AI agents marks a new era in technology, one that holds immense potential for community banking. By leveraging the capabilities of AI agents, Directlink is poised to lead the charge in redefining customer service, operational efficiency, and personalized banking experiences. As we look to the future, the integration of AI agents will undoubtedly play a pivotal role in shaping the next generation of community banking.